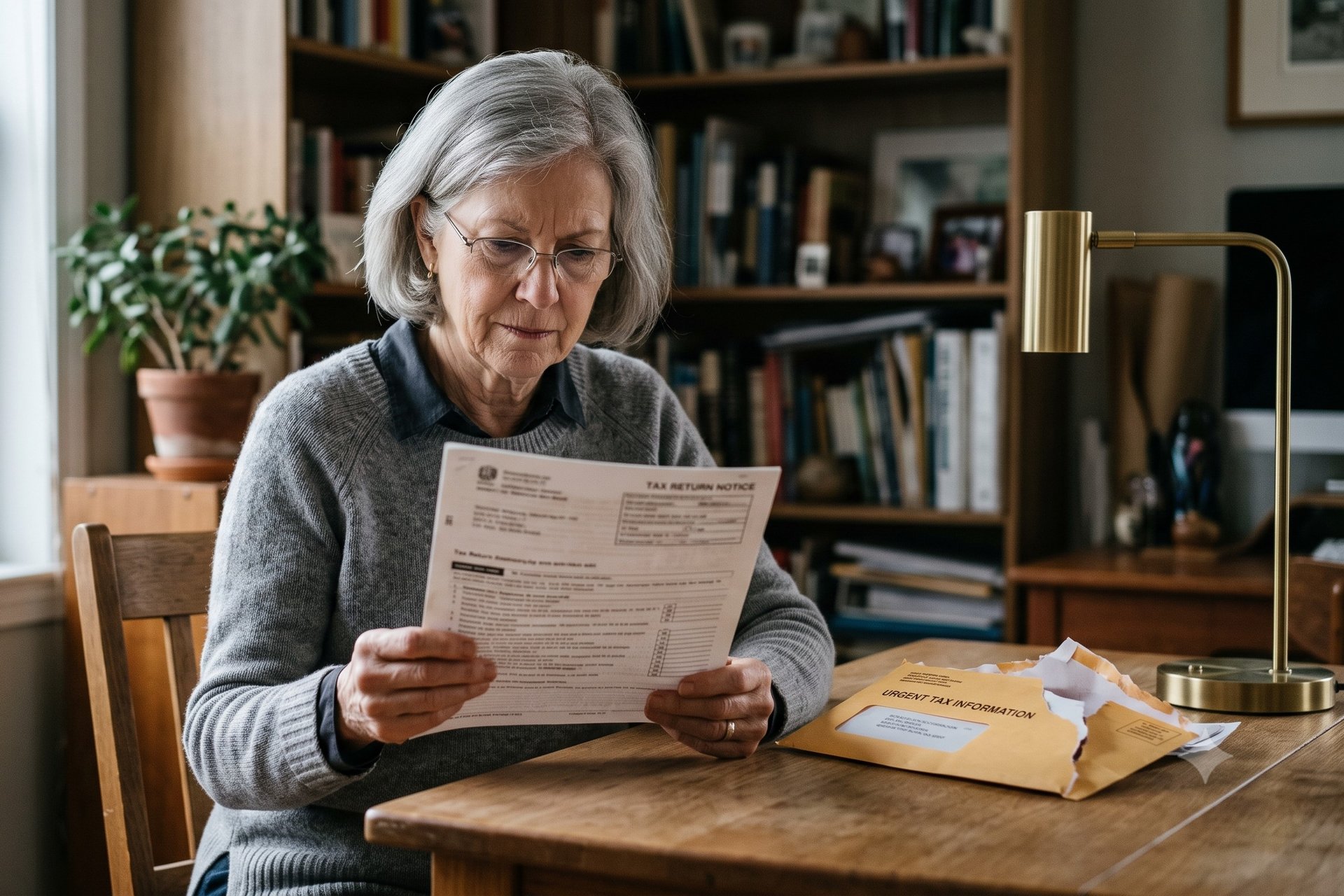

Think about dropping your husband of 45 years in March. Then, the following spring, you open a tax invoice that’s larger than any you paid whereas he was alive — on much less earnings than the 2 of you had collectively.

Merciless? Completely. Uncommon? Not even shut.

I’ve been a CPA since 1981, and I’ve watched this ambush hit widow after widow. It even has a reputation: the widow’s penalty. Virtually no person warns you about it, as a result of it hides inside two guidelines that look unrelated proper up till the day they collide.

Right here’s the excellent news earlier than the dangerous. When you see it coming, you may defuse most of it whereas each spouses are nonetheless alive. However first you’ve received to grasp how the lure springs.

The primary hit: One Social Safety test disappears

When a partner dies, the survivor doesn’t get to maintain each Social Safety checks. The Social Safety Administration helps you to hold the bigger of the 2, and the smaller one merely stops.

So, say your husband collected $2,600 a month and also you collected $1,600. Your $4,200 mixed earnings doesn’t shrink a bit of — it drops to $2,600, flat. That different $1,600 a month, roughly $19,000 a 12 months, is gone for good. (We stroll via how survivor benefits actually get calculated in a separate piece.)

That’s an enormous earnings lower all by itself. However it’s the second hit that basically stings.

The second hit: You’re all of the sudden a single taxpayer

Right here’s the sneaky half. The 12 months your partner dies, you may nonetheless file a joint return. However the 12 months after? Until you’ve received a dependent little one residing at residence — and most retirees don’t — your IRS submitting standing is single.

Single isn’t only a relationship standing. It’s a tax bracket. And it’s a brutal one.

For 2026, a married couple’s commonplace deduction is $32,200. A single filer’s is $16,100 — precisely half. So extra of your earnings turns into taxable the second you’re by yourself.

The brackets are worse, too. In 2026, a married couple stays within the 12% bracket till taxable earnings tops $100,800. A single filer crosses into the 22% bracket at simply $50,400. Similar {dollars}, increased charge.

An actual instance

Let’s isolate simply the filing-status hit. Take $70,000 in taxable earnings and run it via a joint return — the 2026 federal tax is about $7,900. Run that an identical $70,000 via a single return, and it climbs to about $10,100.

That’s roughly $2,200 extra on the exact same earnings, purely as a result of the survivor now recordsdata alone.

Now add in actuality. Her earnings often isn’t the identical — it’s decrease, as a result of that second Social Safety test vanished. But her commonplace deduction simply received lower in half, and her tax bracket additionally shrank.

Backside line? Much less cash is coming in, however a much bigger slice of it’ll the IRS.

Fast apart — most web monetary recommendation comes from individuals who weren’t alive over the past recession. I’ve been writing about cash for greater than 35 years. Need rock-solid recommendation? Sign up for the free Money Talks Newsletter. Takes 10 seconds. No fluff. No spam.

Why this isn’t your fault

When you’re considering you need to’ve deliberate higher, cease. This isn’t a information downside — it’s a design downside. The tax code treats a grieving 78-year-old widow as a brand-new single filer, as if she simply walked in off the road and received her first job.

The system units the lure. Your job is simply to identify it early sufficient to step round it.

5 methods to defuse the widow’s penalty now

The entire recreation right here is to shrink the survivor’s future tax invoice whilst you’re each nonetheless round and nonetheless submitting collectively. Right here’s the place I’d begin.

- Do Roth conversions in your low-income years. Each greenback you progress from a traditional IRA into a Roth IRA whilst you’re in these vast married brackets is a greenback the survivor can later pull out tax-free. The stretch between retiring and beginning required minimal distributions is prime time for this.

- Let the upper earner’s Social Safety develop. Delaying the larger test towards age 70 doesn’t simply enhance your earnings as a pair. It completely raises the survivor profit, which softens that first hit. There’s extra on how claiming works for married couples value studying.

- Change the place your cash lives. If almost all the pieces sits in a standard IRA, the survivor faces massive, totally taxable required minimum distributions at single charges. Build up Roth and common brokerage cash now offers them room to manage their taxable earnings later.

- Be strategic within the 12 months of dying. That’s the final 12 months for a joint return. Promoting an appreciated asset or doing a conversion in that remaining joint 12 months can price far lower than doing the identical factor a 12 months later at single charges.

- Get your affairs in a single place. The survivor can be making tax calls in a fog of grief. A clear file of accounts, passwords, and your tax professional’s quantity retains them from stumbling into avoidable, costly errors.

None of this makes dropping a partner any simpler. However the widow’s penalty is likely one of the few items of that nightmare you may really plan round. Deal with it now, whilst you’re each right here, and also you spare the particular person you like a gut-punch on high of the grief.

That’s a present value giving.

Trending Merchandise